Most investors see the S&P 500’s proven 10.59% average return and assume vacation rental investments can’t compete with stock market returns. A vacation rental showing 8% ROI looks weaker until you realize you only put 20% down. That same 8% becomes a very different number when the bank’s money amplifies your returns, rental income arrives weekly instead of quarterly, and the IRS lets you depreciate a building that’s actually appreciating. Let’s look at what really happens when you put $100,000 into each investment and track the actual wealth outcomes over time.

TLDR:

- Vacation rentals deliver 8-12% annual ROI but borrowed capital multiplies returns to 25%+ on your cash

- You earn monthly income plus property appreciation, mortgage paydown, and tax deductions

- Professional management lifts revenue 23% over competitors and 56% over self-managed properties

- Stocks offer instant liquidity; rentals require $40K-$100K down and active oversight

- AvantStay manages 2,300+ properties with AI pricing and end-to-end operations for passive income

How Borrowed Capital Amplifies Vacation Rental Returns

Real estate’s secret weapon isn’t the headline return percentage. It’s the ability to control a large asset with a relatively small down payment.

Put 20% down on a $500,000 vacation rental, and you’ve invested $100,000. If that property appreciates 5% annually, you earn $25,000 in appreciation the first year. That’s a 25% return on your actual cash investment, not 5%. Buy stocks with that same $100,000, and a 5% gain nets you $5,000.

Borrowed capital multiplies your return potential in ways equity investing simply cannot match. Stock traders can access margin accounts, but borrowing against your portfolio typically means higher interest rates, strict maintenance requirements, and margin calls during market downturns.

Mortgage financing for investment properties offers fixed rates, predictable payments, and no risk of forced liquidation during temporary price dips. You’re using the bank’s money to amplify your wealth-building capacity while rental income covers the loan.

Cash Flow vs Capital Appreciation: Two Different Income Strategies

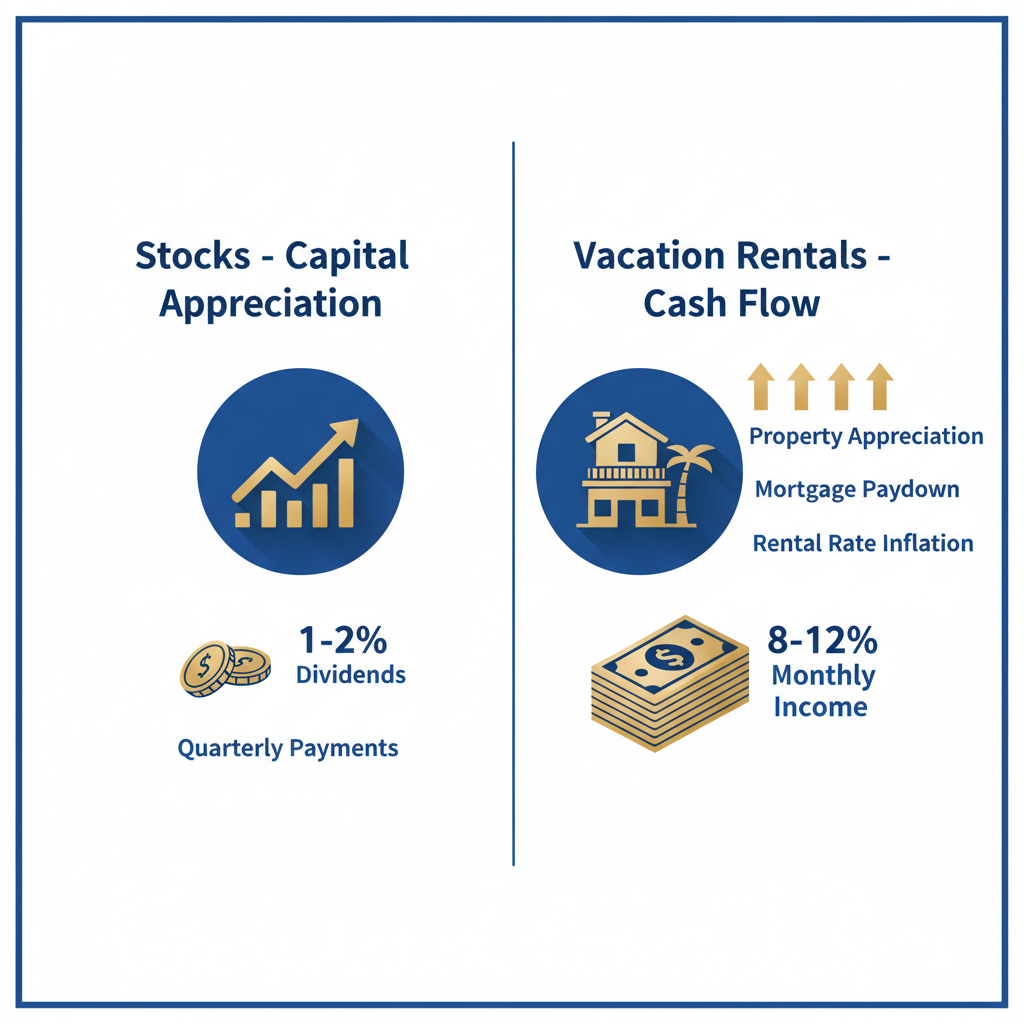

Stocks and vacation rentals generate wealth through opposite mechanisms. Stock investors typically receive modest dividend yields between 1% and 2% annually, with the bulk of returns coming from price appreciation over time. You’re waiting for someone else to pay more for your shares than you did.

Vacation rentals flip that equation. The property generates immediate cash flow every month, with typical cash-on-cash returns between 10% and 15% in well-managed markets.

But here’s the dual benefit: while you’re collecting monthly rental income, you’re simultaneously building equity three ways. Property appreciation increases your net worth. Tenants pay down your mortgage principal each month. Rental rate inflation keeps pace with or exceeds general inflation.

A dividend stock pays you quarterly. A vacation rental pays you weekly while building your balance sheet.

Tax Advantages: Depreciation and Deductions That Stocks Can’t Match

The tax code treats vacation rentals far more favorably than stock portfolios, and the difference can swing mediocre returns into exceptional ones.

When you own a rental property, the IRS lets you depreciate the building over 27.5 years. Buy a $500,000 property with $400,000 attributed to the structure, and you deduct roughly $14,500 annually against your rental income, even though the property value likely increases over time. That’s a paper loss that shields real cash flow from taxation.

Then come the business deductions. Mortgage interest, property management fees, maintenance, repairs, utilities, insurance, HOA dues, and even your travel costs to visit the property all reduce your taxable income.

Stock investors get none of this. When you sell shares for a profit, you pay capital gains tax on the full appreciation. Dividend income? Taxed each year it’s received.

Market Volatility and Risk Profiles

Stock market corrections can erase 30% to 40% of your portfolio value in months. The 2022 bear market dropped the S&P 500 nearly 25% in a single year, and recovery timelines vary widely depending on when you need to sell.

Vacation rental values decline more slowly during recessions. Property prices adjust over quarters or years instead of hours, and rental income keeps flowing even when property values dip. Travelers still take vacations during economic uncertainty.

Real estate carries risks stocks avoid entirely. You can’t sell a property in minutes when you need cash. Problem guests, unexpected repairs, and seasonal vacancy gaps create management headaches that stock investors never face. Local regulation changes or oversupply in your specific market can crater returns while the broader real estate market thrives.

Stocks offer instant liquidity and automatic diversification across thousands of companies. Vacation rentals tie up capital and concentrate risk in a single asset and location.

Investment Factor | Vacation Rentals | Stock Market (S&P 500) |

|---|---|---|

Average Annual Return | 8-12% property ROI, but 25%+ return on actual cash invested when leveraged with 20% down payment | 10.59% average historical return with no leverage benefit |

Leverage Opportunity | Control $500,000 asset with $100,000 down payment; borrowed capital multiplies wealth-building capacity with fixed-rate financing | Margin accounts available but with higher interest rates, strict maintenance requirements, and forced liquidation risk during downturns |

Income Generation | 10-15% cash-on-cash returns with weekly rental payments plus simultaneous equity building through appreciation, mortgage paydown, and rental rate inflation | 1-2% dividend yields paid quarterly; wealth primarily from price appreciation over time |

Tax Advantages | Depreciate building over 27.5 years (roughly $14,500 annual deduction on $400,000 structure); deduct mortgage interest, management fees, maintenance, insurance, and travel costs | No depreciation benefits; capital gains tax on full appreciation when sold; dividend income taxed annually |

Volatility and Risk | Property values adjust slowly over quarters or years; rental income continues during value dips; travelers still vacation during economic uncertainty | Can lose 25-40% of portfolio value in months during corrections; 2022 bear market dropped S&P 500 nearly 25% in single year |

Minimum Capital Required | $40,000-$100,000 for 20-25% down payment plus closing costs, furnishings, and cash reserves | Start with $100 through fractional shares; instant diversification across 500 companies |

Management Requirements | Self-managed requires 5-15 hours weekly; professional management costs 20-30% of revenue but AvantStay handles all operations for passive income | Nearly zero ongoing effort with index funds; set up automatic contributions and portfolio grows passively |

Diversification | Returns depend on single property in one neighborhood; location selection determines success; concentration creates both higher risk and higher reward potential | Spread across 500 companies in different industries and geographies; automatic protection from single-company or sector failures |

Capital Requirements and Barriers to Entry

The entry threshold separates these investment paths in a major way. You can buy fractional shares of an S&P 500 index fund with $100 through apps like Robinhood or Fidelity, building a diversified portfolio across 500 companies immediately.

Vacation rentals demand substantially more upfront capital. A typical investment property requires 20% to 25% down, which translates to $40,000 on a $200,000 property or $100,000 on a $500,000 home. Then add closing costs, furnishings, initial marketing expenses, and cash reserves for maintenance emergencies and vacancy periods.

This concentrated capital requirement creates both opportunity and risk. Stock investors spread $50,000 across dozens of companies instantly. Vacation rental investors commit that same amount to a single property in a single neighborhood, magnifying both potential gains and exposure to location-specific downturns.

Active Management Requirements vs Passive Investing

Stock market investing requires almost zero ongoing effort. Buy an index fund, set up automatic monthly contributions, and your portfolio grows without you lifting a finger. No midnight calls, no broken pipes, no guest complaints.

Vacation rental ownership demands active participation. Self-managed properties consume 5 to 15 hours weekly coordinating cleanings, responding to guest messages, scheduling repairs, stocking supplies, and handling booking logistics. Miss a maintenance issue or delay a response, and your reviews suffer immediately.

At AvantStay, we handle every day-to-day detail so owners stay completely hands-off while properties generate income. Our teams manage guest communication, cleaning coordination, maintenance requests, and pricing optimization through our Voyage system.

The time trade-off matters more than most investors initially recognize. A W-2 professional earning $150 per hour might spend 10 hours monthly managing a rental property. That’s $1,500 in opportunity cost, which can eliminate the cash flow advantage over dividend stocks entirely for smaller properties.

Market-Specific Performance: Location Dependency vs Broad Market Exposure

An S&P 500 index fund spreads your money across 500 companies operating in different industries, geographies, and economic cycles. When tech stocks stumble, healthcare might rally. When U.S. markets decline, international revenue streams provide cushion. You own a slice of the entire American economy.

Vacation rental investors face the opposite reality. Your returns depend entirely on one property in one neighborhood in one city. If tourism demand drops in your specific market, your income disappears regardless of how well rentals perform nationally, making low season marketing strategies critical. The short-term rental industry reached $68.64 billion in 2024 and projects 7.4% annual growth through 2030, but those aggregate numbers mean nothing if your local market tanks.

Location selection becomes everything. A property in Palm Springs benefits from Coachella festival demand and winter snowbird migration patterns that don’t exist in other desert markets, just as Breckenridge properties benefit from ski season demand. Pick the wrong micro-market within the right city, and you watch competitors thrive while your occupancy struggles.

This concentration cuts both ways. Stock diversification protects you from catastrophic loss but caps your upside. Vacation rental concentration exposes you to local risk while offering outsized returns when you choose correctly.

How AvantStay’s Revenue Optimization Changes the Return Equation

Professional management separates theoretical vacation rental returns from what actually hits your bank account. The difference between a self-managed property and one optimized by experts can determine whether vacation rentals outperform stocks or underperform them entirely.

Our Voyage pricing engine analyzes thousands of data points to calculate 75 to 150+ micro-seasons per property through advanced revenue management techniques. While amateur hosts set static nightly rates or make occasional manual adjustments, Voyage pushes ADR increases up to 178% during peak demand windows and strategically reduces rates 15% to 20% during slow periods to lift occupancy. The result: AvantStay-managed properties outperform comparable luxury vacation rental managers in revenue by 23% and net a 56% boost over self-managed properties.

That performance gap changes the entire return calculation, which is why choosing the right management company matters so much. A self-managed property generating 6% ROI suddenly delivers 9% or higher under professional optimization. When you factor in borrowed capital, that improvement becomes double-digit returns on your actual cash investment.

For investors weighing vacation rentals against stock market returns, we solve the active management burden that keeps many high-net-worth individuals in equities. Our vertically integrated approach handles everything while you track performance through the Lighthouse owner portal, delivering the multiplied returns and cash flow advantages of real estate without the day-to-day headaches.

Final Thoughts on Vacation Rentals Versus Stock Market Performance

Your investment timeline and hands-on tolerance make this decision more personal than financial. The beauty of investment properties for short-term rentals lies in controlling a cash-flowing asset that someone else (your guests) pays off while it appreciates, but only if you choose the right market and manage it well. Stock investors trade that potential for instant diversification and zero maintenance calls.

If you want exposure to real estate without the learning curve or time commitment, professional management turns property ownership into a passive strategy that competes directly with equity returns. The best portfolio probably includes both asset classes in proportions that match your goals.

Most vacation rentals deliver 5-10% annual ROI, but leverage changes everything—with 20% down, a 5% property appreciation becomes a 25% return on your cash investment, while the same $100,000 in stocks earning 5% only nets you $5,000.

You can depreciate the building structure over 27.5 years (roughly $14,500 annually on a $400,000 structure) while deducting mortgage interest, property management fees, maintenance, insurance, and even travel costs to visit your property—none of which apply to stock investments.

Self-managed properties typically demand 5-15 hours weekly for guest communication, cleaning coordination, and maintenance scheduling, though professional management companies handle all operations in exchange for 20-30% of gross revenue.

An S&P 500 fund spreads risk across 500 companies in different industries and regions, while your vacation rental returns depend entirely on tourism demand in one specific neighborhood—the right micro-market can deliver 12%+ ROI while the wrong one struggles regardless of national trends.

Vacation rental properties require 20-25% down payment plus closing costs, furnishings, and cash reserves—translating to $40,000-$100,000 minimum for most investment-worthy properties, compared to starting stock investments with as little as $100 through index funds.